|

|

|

|

Economic Principles: How the Market Works

Chapter 1: Introduction

- History

- Wealth explosion

- Its parallel with freedom

- What can we learn from experience

- Philosophy of the book

To be remembered:

• Smith

• Correlation

• Causality

• Institutions

• Logic of choice

Bibliography:

- Julian L. Simon, The Ultimate Resource, Princeton University Press, 1981. Part of the book is available on line at http://www.juliansimon.com/writings/Ultimate_Resource/

- David Landes, The Wealth and Poverty of Nations: Why some are so Rich and some so Poor, Abacus, 1999

- Deepak Lal, Unintended Consequences, MIT Press, Cambridge Massachusetts, 1999

- Frédéric Bastiat, Selected Essays on Political economy, “What is Seen and What is Unseen”, Irvington-on-Hudson, NY: The Foundation for Economic Education, Inc. 1995

- Gerald p. O'Driscoll, Jr., Kim R. Holmes and Melanie Kirkpatrick, The 2001 Index of Economic Freedom, The Heritage Foundation and the Wall Street Journal.

- Kirzner on Teaching economics

- Adam Smith, An Inquiry into the Nature and Causes of the Wealth of Nations, Indianapolis: Liberty Classics, 1981.

- Johan Norberg, In Defence of Global Capitalism, Timbro 2001. www.timbro.com

- Douglass C. North, Institutions, Institutional Change and Economic Performance, NY: Cambridge University Press, 1990

A Fundamental Question: How do we get a larger choice?

-

As revealed by common language, an economic activity is an activity aimed at improving living conditions, at improving his or her lot, or the life of those one cares about. Needless to say that economic activity is as old as the human condition.

- But throughout history , human beings have been more or less successful in their economic activities. [See Landes' book for a fascinating journey throughout history and a description of how some society have grown reach while others remained poor.]

- Why ? Why have some individuals, some groups, and some civilizations been more successful than others in making a better life for themselves? This is the main question we wish to address in that course.

- What do we mean by success? Of course the notion of “success” is very subjective. For some, to live a quiet life without having to worry too much about how to sustain himself is the definition of success. For others to be successful requires fame and power. Still for others the success consists in bringing some happiness to others. But whatever the chosen goal, it is always a good thing to have more possibilities available. In that sense, more material wealth, more resources are always welcomed. Hence a successful economic activity can be broadly defined as an activity that expands the realm of possible choices through an expansion of resources .

- This question being a fundamental one many thinkers have considered it in the past. But without surprise, it is particularly when it was obvious that some progress was taking place that attempts have been made to provide an articulated answer. It is therefore not by chance that economics as a specific domain of knowledge started to develop in the 17 th -18 th century and in Western Europe where a real wealth explosion was starting.

- This is well illustrated by the fact that it was during that period that appeared what remains one of the best economic analysis ever written, namely, Adam Smith 's “Essay on the Nature and the Causes of the Wealth of Nations” (1776). As indicated by the title of the book, the Scottish Professor was trying to answer two questions: (a). What is the nature of wealth? Or, in the terminology defined above, what do we mean by success? (b). How do we get wealthier? Or, again using our terminology, how do you get successful?

To find an answer we must not trust our intuition

We are all actors of economic life. We consume, we produce, invest and save. This, as we will see throughout the course, is sometimes of great help. It gives us some way to appreciate the theories that are offered by professional economists. Common sense is sometimes helpful to unveil unsoundness in economic theorizing.

But this does not mean that we always have a clear understanding of what is going on. As a matter of fact, our intuition, as far as economic phenomena are concerned, is sometimes misleading. 1 In particular, it is easy when talking about the economy, and more generally about social phenomena, to fell in a trap that consists in giving too much importance to our daily problems.

This is the reason why we hear so many stupid comments on the economy [illustrations].

It also explains why history is important. History forces us to place in perspective our daily experience. Johan Norberg, in a recent book entitled “In Defence of Global Capitalism”, provides many examples of wrong believes which can be easily dismissed just by looking at history. Let me take two of them.

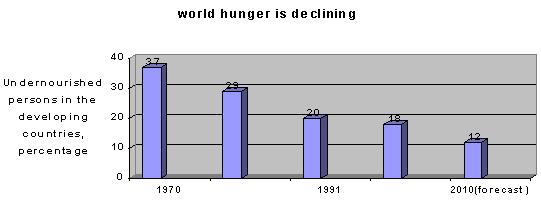

It is often believed, because we see such terrible pictures on our television's screen, that no progress is being made at a world level in the direction of decreased poverty . Data gathered by the United Nations shows however clearly that such is not the case. As a matter of fact, world hunger has been sharply declining over the last forty years. (Norberg, page 31)

Because each day we receive so many reports on the stock market, with new stories about mergers and acquisitions, one easily gets the impression that production is becoming more and more concentrated in the hands of a few big players. This in turn creates worries that the world economy can be directed by a handful of individuals. Looking at the data, we get however a different picture. Hence if you take the 500 largest firms in the U.S.A. for the year 1980 you can see that they represented close to 60% of American GDP. But in 1993, the 500 largest companies accounted for just above 35% of GDP. (See, Norberg, page 202) The point I wish to stress here is that probably few of us were aware that such a trend was taking place in the 1980s because we do not put in perspective the news that are given to us by many medias.

As those two examples illustrate, we must develop a sound attitude with respect to facts, let it be facts of our own life, or facts that are reported to us by various means.

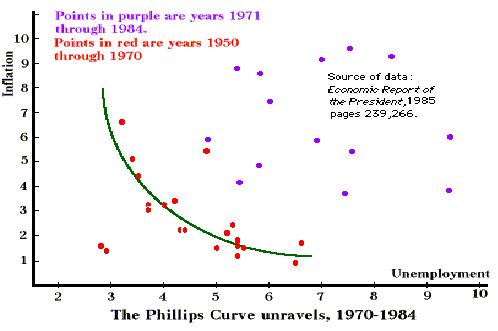

We have stressed the danger to generalize some partial results, or some of our daily experiences. The second main danger is to confuse correlation and causality. Observations, and more generally statistics, indicate some correlations between series of facts. For instance, in the 1950s, an economist (A.W.H. Phillips) has found a clear correlation between inflation and the rate of unemployment. 2 On the graph below this correlation is represented by the red dots. From the observation of this correlation it was easy to deduce that to reduce unemployment it was necessary to accept a higher rate of inflation. As it turns out, that deduction turned out to be wrong. The correlation was exact (at least for a period of time) but the interpretation in terms of causality that was to the correlation was wrong. This is obvious when we look at the blue dotes that give us information between inflation rate and unemployment rate in the following decades: the correlation does not hold any longer, which shows that the interpretation given to early founding was totally misleading.

Another example is provided by the link between Money supply, prices and the level of transactions in the country. That there is a correlation between the total amount of money in the economy, the “general” level of price in that economy and the amount of transactions taking place in the country is almost a truism. 3 The difficulty lies entirely in the identification of the causal links between those aggregates. Can we say that more money causes essentially an increase in the general level of price (i.e., inflation)? Or can we argue, for instance, that more money makes business easier and therefore increases the number of transactions? Both theories ate compatible with the observed correlation. Once again, a correlation is… just a correlation. It can lead you eventually to disregard some theories, it can surely give you some information, but it will not give you a theory. And when someone starts a speech saying “Data show that…”, let us separate cautiously what the data really tell us from the personal interpretation that this person is offering.

Last illustration of the kind of problems raised by data from past experience: the interpretation of the sustained growth in Western European countries following World War II. During almost three decades those countries have enjoyed a relatively high growth of their GDP (Growth Domestic Product). During that period, most Western European governments were convinced of the possibility to “fine tune” the economy with the help of an economic policy constructed along the lines indicated by the famous English economists, John Meynard Keynes. As a consequence governments were largely interfering with the economy (nationalization of some industries, active fiscal and monetary policy, large public investments, etc.). Hence, it is easy to conclude that the choice of an active policy explains the sustained growth. 4 But what data can hardly tell us is whether the growth took place because or in spite of government intervention. It is possible that the cause of the expansion is to be found elsewhere (like, for instance, in the development of international trade that took place in that same period).

The lesson to be drawn from those various examples is that in order to understand what can lead to progress, to a larger choice, one need to look at experience. But at the same time one must remain very cautious when interpreting event from the past. Social sciences in general and economics in particular are complex and our intuition generates shortcuts that are often misleading.

As the French economist of the mid 19 th century, Frédérique Bastiat, out it: 5

In the economic sphere an act, an habit, an institution, a law produces not only one effect, but a series of effects. Of these effects, the first alone is immediate; it appears simultaneously with its cause; it is seen . The other effects emerge only subsequently, they are not seen , we are fortunate if we foresee them.

There is only one difference between a bad economist and a good one: the bad economist confines himself to the visible effect; the good economist takes into account both the effect that can be seen and those effects that must be foreseen .

To find an answer we must look at institutions

The method that will be followed in order to find an answer to our main question—how do we get a larger choice—will be presented in the next chapter. But, it might be helpful to set clearly from the start where that inquiry will lead us. It will lead us to focus on institutions .

By institutions we mean all the more or less stable rules that form the framework in which interactions take place. This includes:

- The legal framework: private law (property rights, liability rules, contract laws, family law), public law, competition law, labour law, environmental laws, etc.

- Monetary institutions (Do we have a central bank with a monopoly in the issue of money? Do we have competing currencies? What are the rules that control credit expansion?)

- International treaties (Do we have free-trade with foreign countries?)

- Political institutions (How do we choose our representatives? Is the government limited in its policies?),

- Taxation rules, etc.

It also includes less formal rules such as tradition, habits. Those traditions and habits will generate Corruption, trust.

Hence, to be a “good” economist it is not enough to understand how individuals make their choices (what one sometimes call “ the logic of choice ”). It is very important to understand how those choices vary according to the context.

This is why many chapters in that course will be dealing with law or political institutions.

The perspective taken in this course (looking at the logic of interactions of choice and beyond that at the emergence and functioning of institutions) is not revolutionary. During the last decades economists have paid increasingly more attention to institutions. Historians have done the same (see n particular the works of the Nobel Prize winner, Douglas North).

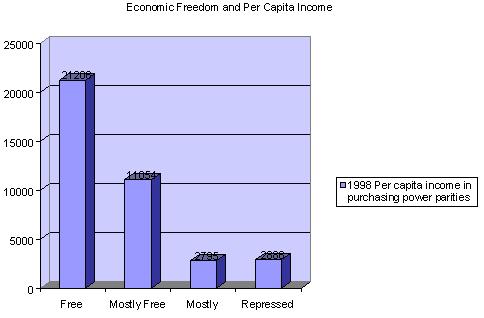

In particular, we will be interested in the link between degrees of freedom and progress. That link has been studied for many years and we now have some statistics worth taking into account. 6 Of course, what has been before regarding statistics applies to those statistics as well, namely they must be taken with care, as a basis for our reflection. You will find below some statistics gathered by the Worl Bank in its 2000 World Development Indicators:

By looking at institutions and degrees of freedom to understand progress we will, in a way, be going back to our roots. Indeed, Adam Smith himself not only was a promoter of economic freedom but also had started his career with a book on the emergence of rules of conduct ( The Theory of Moral Sentiments ), that is to say, with a book on institutions.

----------------------

1 See the short article written by Kirzner in The Freeman , on economic education.

2 To be more exact, the correlation studied by Phillips was between unemployment and the rate of wage inflation. The following graph was found on the following site: http://ingrimayne.saintjoe.edu/econ/Labor/FallPhil.html . For more on the Phillips curve you can vist the following website http://www.cato.org/pubs/tbb/tbb-0205-5.pdf where you will find an articale by W. Niskannen and A. Reynolds on the topic.

3 I am here oversimplifying the issue. Indeed, it is not easy, and surely potentially dangerous, to define a “total money supply” or “a general level of price”. But for the present purpose it is enough that some economists—actually, most economists—think that those concepts make sense.

4 In the same manner, the American economist of the 19 th century, Henry Carey, believed that protectionism was the cause of American expansion.

5 The all essay can be found at : http://www.econlib.org/library/Bastiat/basEss.html

6 see for an example the “2001 Index of Economic Freedom” published by The Heritage Foundation and The Wall Street Journal and available on line at http://www.heritage.org/research/features/index/2001/